For many service members and families, the Thrift Savings Plan sits quietly in the background, something you know you should pay attention to, but rarely take the time to dig into. Between PCS moves, deployments, training cycles, the everyday demands of life, and the feeling that retirement seems forever away, it tends to take a back seat to all the other things going on in life. The truth is, the TSP is one of the most powerful wealth-building tools you have, and you don’t need a finance degree to understand how it works, just a clear explanation and a few smart decisions. Let’s look at some common and maybe not-so-common questions about TSP…

What IS the Thrift Savings Plan?

- The Thrift Savings Plan (TSP) is the federal government’s version of a 401(k), a retirement savings account that allows you to invest money in now, so it grows over time.

- For service members in the Blended Retirement System, the TSP is an integral part of your retirement package, complete with automatic contributions and potential matching from the Department of Defense.

Why the TSP Matters for Military Members

- Retirement investing can be confusing. The TSP is designed to simplify planning, offering low fees, simple investment options, and the flexibility to continue contributing whether you’re stateside, deployed, or transitioning out of the service.

- Since your career path may include PCS moves, breaks in service, or early separation, the TSP gives you a portable, long‑term financial foundation that stays with you no matter where the military sends you.

How does the TSP work?

- Think of it as a partnership between you and your future self.

- You choose how much to contribute from your paycheck, and that money goes into your TSP account.

- If you’re in the Blended Retirement System, the DoD also contributes automatically and may match part of what you put in.

- Over time, your contributions and investment growth compound, meaning your money earns money.

What are my contribution options (Traditional vs. Roth)?

- The TSP offers tax-advantaged savings in two ways:

- Traditional TSP: You don’t pay taxes on the money now, the money grows tax-deferred, and you pay taxes on the amount contributed and the growth when you withdraw it in retirement.

- Roth TSP: You pay taxes on the contribution amount now, and the investment grows tax-free. Withdrawals in retirement are tax‑free if you follow the rules.

- Both options can be smart—it just depends on your situation and goals.

What are the TSP investment funds?

- The TSP keeps things simple.

- Instead of hundreds of choices, you get a small menu of funds that represent different parts of the market.

- These include the G, F, C, S, and I Funds, plus the Lifecycle (L) Funds that mix them automatically based on your target retirement date.

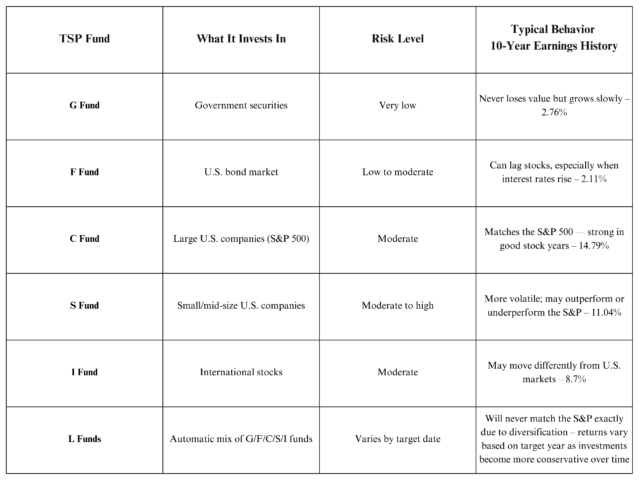

What does each TSP fund invest in?

- Here’s a quick overview of the different fund options, what each invests in, the level of risk, and how the funds have performed over the past decade:

- Each fund represents a different “slice” of the market and mixing them helps balance risk and reward.

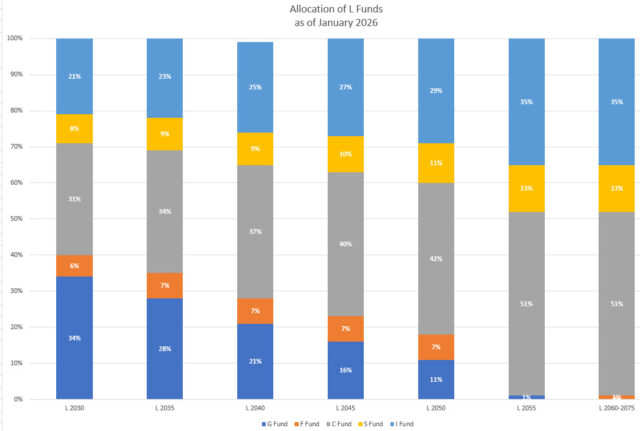

How do the Lifecycle (L) Funds work?

- L Funds are “set it and forget it” options.

- You pick the fund closest to the year you expect to retire, and it automatically adjusts your mix of investments over time—more growth when you’re younger, more stability as you get closer to retirement.

How do I choose the right TSP fund for my goals?

- Start with two questions:

- How long until I need this money?

- How comfortable am I with ups and downs in the market?

- Longer timelines usually allow for more growth‑focused funds (C, S, I).

- Shorter timelines or lower risk tolerance lean toward more conservative options (G, F).

- L Funds are a great middle ground if you want simplicity.

How much should I contribute to my TSP?

- A good starting point is enough to get the full DoD match if you’re in the Blended Retirement System.

- From there, increasing your contribution by even 1% each year can make a huge difference over time.

- Investing early in your career enables greater growth opportunities.

- The key is consistency.

What happens to my TSP if I PCS, deploy, or leave the military?

- Your TSP stays with you.

- You can keep contributing while deployed, and if you separate or retire, the account remains yours.

- You can leave it where it is, roll it into another retirement account, or start withdrawing in retirement, typically age 59 1/2.

How do I check or change my TSP allocations?

- You can log into your TSP account online and adjust your contributions or investment choices anytime.

- It’s quick, and even small changes can help you stay aligned with your goals.

What mistakes should I avoid?

- A few common ones:

- Not investing at all.

- Leaving money on the table by not contributing enough to receive the government match.

- Putting everything in the G Fund because it “feels safe.”

- Forgetting to update contributions after a PCS or promotion.

- Trying to time the market.

- Slow, steady, and consistent usually wins.

How can the TSP help me build long‑term wealth?

- The combination of low fees, matching contributions, and decades of compound growth makes the TSP a powerful engine for your financial future.

- Even modest contributions can grow significantly over a military career.

Where can I learn more or get help?

- The TSP website is the go-to source for TSP information.

- Your installation’s financial readiness office and Military OneSource are excellent sources for personalized TSP assistance.

- The more you understand, the more confident you’ll feel about the choices you’re making.

Find Out More with My Military Savings and Finances!