Debt comes in many forms, credit cards, car loans, student loans, mortgages, and consumer loans. You can buy anything on credit today, and that can be dangerous if you don’t have a plan for the debt, and its elimination. Debt can allow us to buy things we need and want without having to wait and save for them. We need to be careful with debt, as payments, and the resulting interest, takes away other options and uses for our money.

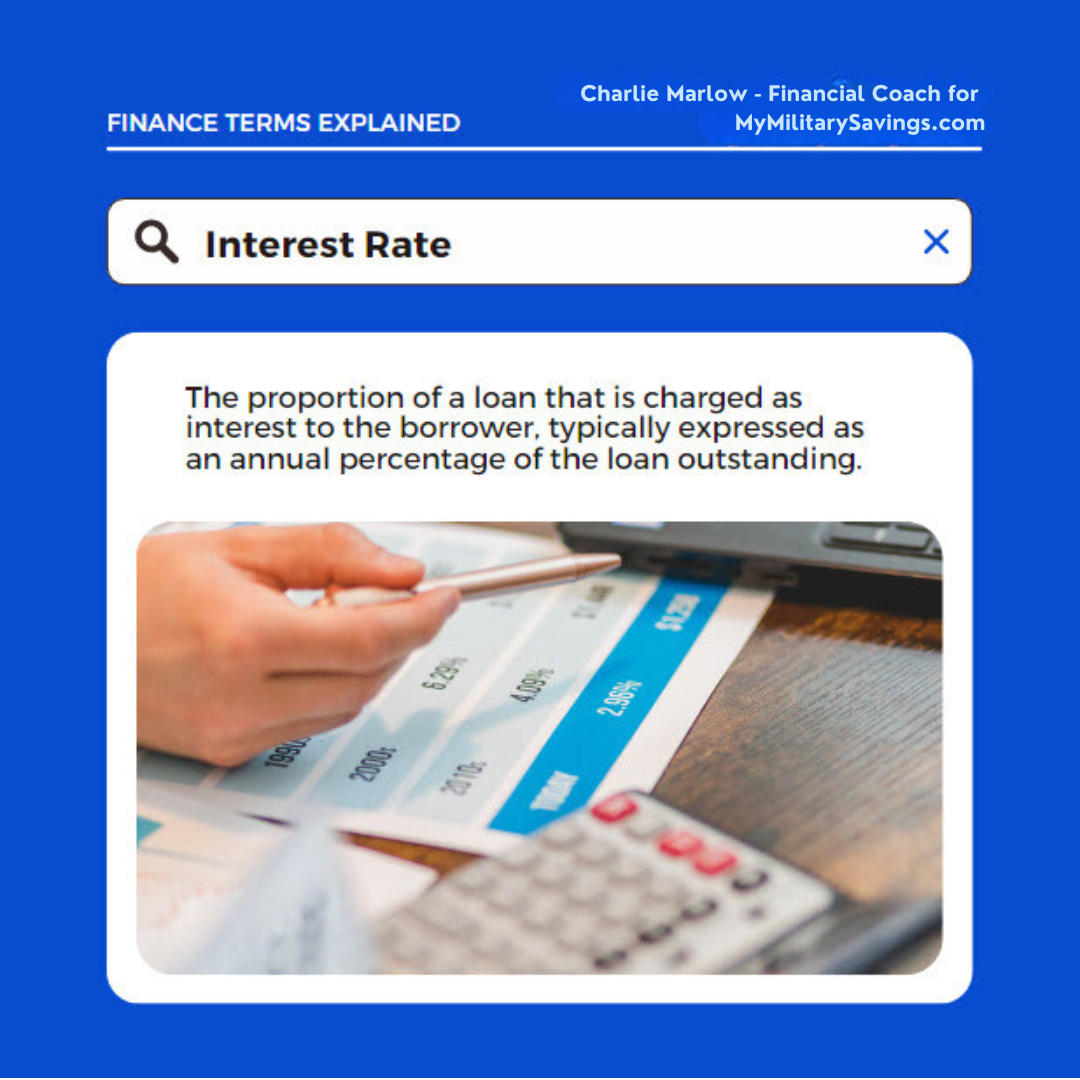

Interest is the “rent” we pay on the money we’ve borrowed. Depending on the debt amount, the interest rate, and the time we are in debt, the amount of interest we will pay is on top of the purchase amount. The higher the interest rate, the more you’ll pay for borrowing the money.

If you borrow $1,000 at 10% for 6 months, you’ll pay a total of $29.36 in interest. If you spread it over 12 months, the total interest comes to $54.99. On large loans, such as a home, the interest paid over the life of the loan can be as much or more than the principal amount borrowed. A $400,000 home with a 30-year, 5% interest rate, will result in a total of $373,021 paid in interest.

Borrow carefully!

Find Out More with MyMilitarySavings.com and Finances!

Add comment