A new federal savings tool for children—Trump Accounts—is set to launch in 2026, with important implications for military families. Under the One Big Beautiful Bill Act, eligible children can receive a one‑time $1,000 federal pilot contribution, but only if a parent or guardian files IRS Form 4547 during the 2026 tax season.

For military households navigating PCS moves, deployments, and the unique rhythms of service life, understanding how this new account works can help you build long‑term financial stability for your children, no matter where the military sends you.

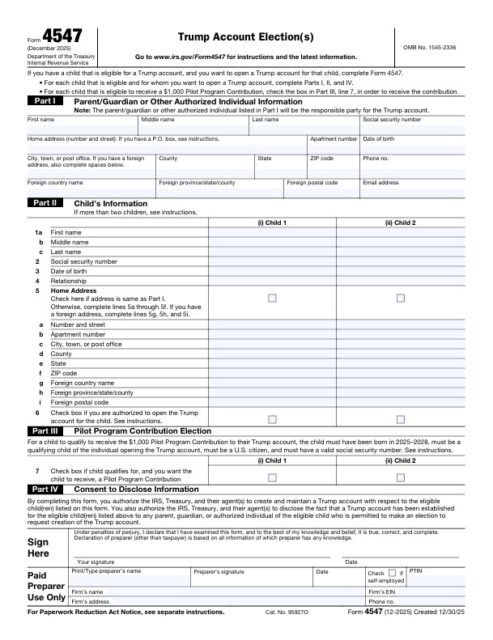

What IRS Form 4547 Does

- Form 4547 is the official election form that:

- Opens a Trump Account for a child under age 18

- Requests the $1,000 federal seed contribution for eligible children born 2025–2028

- This form is filed during the 2026 tax season, alongside your 2025 return.

Who Can File (Important for Deployed or Geographically Separated Families)

- The following individuals may file Form 4547:

- A parent

- A legal guardian

- In certain cases, an adult sibling or grandparent

- To receive the $1,000 contribution, the filer must also claim the child as a dependent.

- This matters for military families because:

- If one parent is deployed, the at‑home spouse can still file.

- If a child is living temporarily with grandparents during a PCS or deployment, the dependency rules still determine who can claim the $1,000.

- Dual‑military families should coordinate who claims the child to avoid delays.

Who Qualifies for the $1,000 Pilot Contribution

- A child must meet all of the following:

- Born January 1, 2025 – December 31, 2028

- U.S. citizen with a valid Social Security number

- Lives with you and is claimed as your dependent

- Has not already received the pilot contribution

- Children outside this birth window can still open a Trump Account—they simply won’t receive the $1,000 seed deposit.

- Key Dates Military Families Should Track

- January 2026: Filing season opens

- April 15, 2026: Tax deadline (extensions still available for deployed members in combat zones)

- May 2026: Activation instructions sent

- July 4, 2026: Contributions begin and federal deposits start

- For service members deployed to a combat zone, the IRS typically extends filing deadlines. That means you may have additional time to submit Form 4547 without penalty.

Contribution Limits

- $5,000 per year from family

- $2,500 per year from employers

- Unlimited philanthropic contributions

This structure allows military families to:

- Build savings even during lower‑income years

- Invite grandparents or extended family to contribute

- Use employer contributions if your service‑connected civilian employer offers them (may apply for some Guard/Reserve families)

Trump Account vs. 529 Plan: Which Fits Military Life?

- Both accounts can work together, but they serve different purposes.

- Trump Account

- General long‑term savings

- Usable after age 18

- Not restricted to education

- Portable across states and duty stations

- 529 Plan

- Education‑focused

- Tax‑free for qualified education expenses

- Can be used for college, trade school, or certain K–12 tuition

- Also portable across states

- For military families who move frequently, the portability of both accounts is a major advantage. A Trump Account can serve as a flexible “launch fund” for adulthood—useful for first‑car purchases, emergency savings, or early career expenses—while a 529 remains the go‑to tool for education.

- Trump Account

Why This Matters for Military Families

- Military life creates unique financial challenges:

- Frequent PCS moves disrupt employment and savings

- Deployments create periods of separation and logistical complexity

- Childcare and school transitions vary by duty station

- Many families support children through long-distance parenting

- A Trump Account offers:

- A federally backed starting point for long‑term savings

- A predictable contribution window

- A way for extended family to support children even when parents are deployed

- A tool that stays with the child regardless of where the military sends you

- For junior enlisted families especially, the $1,000 pilot contribution can be a meaningful jump‑start to long‑term financial security.

Find Out More with My Military Savings and Finances!