Charlie Marlow – Financial Coach

What is TSP? – The Thrift Savings Plan (TSP) is the retirement savings and investment vehicle for federal government employees and members of the uniformed services. Established by Congress in 1986, the TSP offers a service similar to private sector 401k plans. It allows you to set aside money for retirement in a wide selection of funds to meet your savings goals, timeframes, and risk tolerance.

How much can I contribute? – Employees and military members may contribute up to $23,000 in 2024. If you’re 50 or older you may also contribute additional “catch-up” contributions of up to $7,500. Military members assigned to a tax-exempt zone can make traditional tax-exempt contributions. The total that may be made is $69,000 including Traditional and Roth contributions, employer/agency matches, and tax-free combat zone contributions. The $69,000 does not include any catch-up contributions.

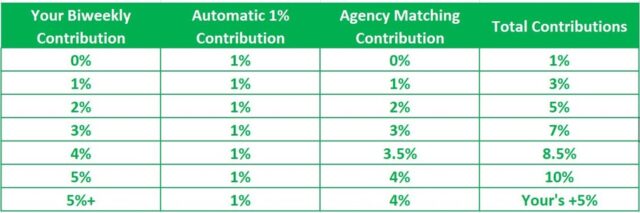

Is my contribution matched? – Military members who are enrolled in the Blended Retirements System (members with a Date of Initial Entry into Military Service (DIEMS) date of January 1, 2018, or later or eligible members with a DIEMS date of December 31, 2017, or earlier who elect (opt in) to be covered by BRS) will receive an automatic contribution of 1% of their basic pay from the DoD beginning 60 days from enrollment. After two years of service, the DoD will also match the service member’s contribution through the end of their 26th year of service. The DoD matches your contribution dollar for dollar for the first 3% then 50 cents per dollar for the next 2%.

What are my investment options? – TSP offers five different types of individual funds, each with its own objectives, risks, and associated expenses. TSP also offers 10 different Lifecycle Funds that are mixes of the five individual funds, based on your anticipated retirement date, and managed to periodically grow less aggressive and more conservative as you approach retirement like how commercial target date funds work.

Individual Funds

G Fund – Government Securities Investment Fund – The objective is to ensure the preservation of capital and generate returns that are higher than what you can get through short-term U. S. Treasury securities. This is the safest of the funds because the fund’s principal and interest are guaranteed by the U. S. Government. This investment carries inflation risk, the possibility that the returns will not keep pace with inflation and reduce purchasing power.

F Fund – Fixed Income Index Investment Fund – The objective is to generate higher returns than available in short-term securities like the G Fund by investing in debt instruments like bonds issued by governments and corporations to generate income. The fund is designed to match the performance of the Bloomberg U. S. Aggregate Bond index. Bond investments carry market risk because the investments can fluctuate in value, credit default risk because the issuer may not be able to pay their debt, and inflation risk because the earnings may not be enough to offset inflation.

C Fund – Common Stock Index Investment Fund – This fund aims to offer the opportunity to gain from the equity ownership of stock in a broad market of large and mid-sized U. S. companies. The fund is designed to match the performance of the Standard and Poor’s (S&P 500) Index. This fund has market risk as the value of stocks rise and fall and inflation risk if the investments do not outpace inflation.

S Fund – Small Cap Stock Index Investment Fund – The objective of this fund is to offer the opportunity to experience the gain from the equity in small to mid-sized U.S. companies. This fund is designed to match the Dow Jones U. S. Completion Total Stock Market Index. As with other stock-based investments, this fund also carries market and inflation risk.

I Fund – International Stock Index Investment Fund – This fund offers the opportunity to invest in the ownership of non-U. S. companies and represents many developed countries. This fund’s objective is to match the returns of the MSCI EAFE (Europe, Australasia, Far East) Index. Risks include currency risk, the fluctuation of the value of foreign currencies in relationship to U. S. currency as well as market and inflation risk.

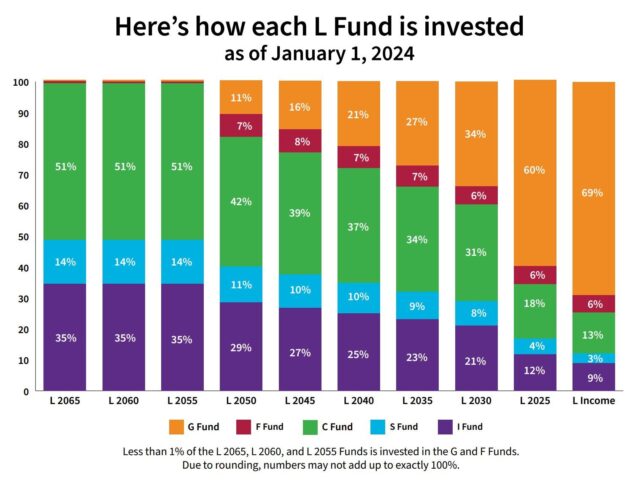

Lifecycle Funds

There are 10 Lifecycle Funds, each with a diversified mix of the five individual funds designed to get the best-expected return for the risk appropriate for your age. The 10 funds are named for the target year closest to your retirement date: 2025, 2030, 2035, 2040,2045,2050,2055,2060, and the L Income Fund. Once the year of the fund date is reached, the funds are rolled into the L Income Fund. Funds are reallocated each quarter to a lower-risk profile.

What are the taxability options? – There are two types of tax treatment for your TSP, regardless of which funds you select, Traditional and Roth. Traditional contributions are made pre-tax and reduce your taxable income in the year of the contribution. Traditional contributions reduce your current year’s tax in the year of contribution and grow tax-deferred until withdrawal when all withdrawals, including contribution and growth, are taxed in retirement. Roth contributions are made with after-tax dollars, do not offer a tax break, but grow tax-free until retirement. Roth withdrawals are not taxed in retirement.

Find Out More with MyMilitarySavings.com and Finances!

Add comment